B.C. Has Been Here Before: The Long History of Land Value Taxation in British Columbia

By Liam Wilkinson | May 11, 2026

Summary

British Columbia was once one of the world’s leading land value tax jurisdictions. By 1914, roughly two-thirds of B.C. municipalities had adopted some form of site-value or land-value taxation.¹

Vancouver had a form of land value tax from 1910 to 1984, according to a 2018 Vancouver council motion later included in the city’s land value capture review.²

The ideas of Henry George were central to this policy landscape, but LVT was also practical. George’s ideas shaped reformers, labour activists, planners, and later figures such as Bob Williams and Ted Gwartney. But B.C.’s early LVT systems also emerged because municipalities needed revenue and wanted to discourage land speculation.³

BC Assessment is a crucial part of the story. It was formally created in 1974 to provide fair, independent, province-wide property assessment, and a possible bridge to land value capture.⁴

Habitat I, hosted in Vancouver in 1976, put land value capture on the world stage. The Vancouver Action Plan recommended that publicly created increases in land value be recaptured for the community in the form of a Land Value Tax.⁵

Recent municipal interest has appeared through grassroots and local government advocacy. Victoria, Vancouver, and the Union of B.C. Municipalities have all explored or endorsed versions of land value taxation, vacant land taxation, or land value capture in recent years.⁶

The idea that keeps coming back

Long before housing prices dominated B.C. politics, British Columbians were already asking a familiar question: when land values rise because of public investment, public decisions, and community growth, who should benefit?

Today we talk about land lift, speculation, development charges, community amenity contributions, upzoning, transit-oriented development, and housing affordability. A century ago, many British Columbians approached that same problem through a different phrase: the single tax.

The phrase came from the movement inspired by Henry George, the American political economist whose 1879 book Progress and Poverty became one of the most influential reform texts of the late nineteenth century. George argued that rising land values were not produced by individual landowners alone. They reflected the growth of the community around them: roads, railways, ports, schools, water systems, public decisions, and the growing demand for access to good locations.

His remedy was land value taxation. Tax land, not buildings or labour. Tax the value created by nature and society, not the homes, shops, factories, and improvements people build through effort and investment.

As a 1913 study of land taxation in Western Canada put it, George proposed that the public should reappropriate for itself “the rental value of natural opportunities.”⁷

That idea travelled far. It influenced reformers in the United States, Britain, Australasia, and Canada. In Britain, land valuation became part of the politics around the Lloyd George Budget of 1909. In Australasia, land taxes were used to challenge large estates. In Western Canada, the idea found a particularly receptive audience in fast-growing cities where land speculation was not an abstract theory, but a visible fact of urban life.⁸

Why B.C. was fertile ground

British Columbia was built through land decisions. Railway land grants, monopoly resource rights, vast timber holdings, coal lands, townsite speculation, agricultural settlement, Indigenous dispossession, and rapid urban growth all shaped the province’s early political economy.

It is not surprising, then, that the land question quickly became central to the new political consciousness emerging through labour organizing.

Thomas Loosmore’s history of early B.C. labour politics notes that workers objected to the alienation of land and resources to corporations such as the Esquimalt and Nanaimo Railway Company and the Canadian Pacific Railway. In response, many were “strongly attracted” to the single tax.⁹

The politics of the era were complicated. Georgism was influential, but it existed alongside labour organizing, direct democracy, socialism, anti-monopoly politics, public ownership, and, notably, anti-Chinese exclusionary politics. The single tax was one strand in a period of rapidly evolving political experimentation.

By the 1890s, B.C. municipalities were also gaining the legal tools that made land value taxation possible. They acquired the power to distinguish land from improvements in their assessment systems. That distinction is the foundation of land value taxation: once land and buildings are assessed separately, governments can choose to tax them differently.

Stalker’s 1913 study described this as a gradual evolution in B.C.’s municipal system. The province had slowly extended local autonomy until municipalities had broad power over “the taxation of land values and the exemption of improvements.”¹⁰

B.C.’s first land value tax era

By the early twentieth century, B.C. had moved from debate to practice.

Between 1903 and 1914, Western Canada shifted strongly toward site-value taxation. A 1994 CMHC study by Mohammad Qadeer and Andrejs Skaburskis found that, by 1914, about two-thirds of B.C. municipalities had adopted the method.¹¹

Stalker’s near-contemporary account gives a fuller picture of how quickly the policy spread. He wrote that land value taxation had been adopted by more than fifty B.C. municipalities, many of which were exempting improvements to varying degrees. The list included Vancouver, Victoria, South Vancouver, North Vancouver, Nanaimo, Prince Rupert, New Westminster, and Kelowna. Victoria and New Westminster adopted the complete exemption of improvements in 1911.¹²

Vancouver became the best-known example. A century later, Vancouver council would state plainly that the city “had a Land Value Tax from 1910 to 1984.”¹³

Still, this was not the single tax in Henry George’s full sense. Much of Western Canada adopted some form of land value taxation, but not always as a direct application of George’s teachings. In many cities, it developed as a practical municipal tool: a way to raise revenue, reduce the tax burden on buildings, and respond to speculation in rapidly growing urban centres.¹⁴

Vancouver and the Limits of Land Value Taxation

Vancouver is one of the most important case studies from this period.

By 1911, the city raised about 79 percent of its municipal revenue from land. That made Vancouver one of the most significant land-tax jurisdictions in North America, but it was still not the full single-tax system imagined by Henry George’s most committed followers. When federal, provincial, and municipal taxes were counted together, land taxes represented about 43.5 percent of Vancouver’s total estimated public revenue collection.¹⁵

The system also had limits. By 1913, Stalker reported that Vancouver was already facing significant revenue pressure. The assessment roll had not grown fast enough to keep pace with the city’s rising expenditures, and council faced a choice: raise the land-tax rate or restore some taxation of improvements.¹⁶

Vancouver chose the latter. Rather than continue increasing the visible tax rate on land, with all the political and investment concerns that came with it, the city began expanding the tax base by bringing buildings back into taxation.

A similar pattern appeared across Western Canada. The CMHC study found that land value taxation had some success in pushing underused land toward development and breaking up large holdings. But it did not end speculation, boom-bust cycles, or sprawl. After the First World War, improvements again became a more important municipal tax base as cities grew and needed more stable revenue for services and infrastructure.¹⁷

This is one of the most important lessons from the B.C. record: land value taxation was not a magic switch. It was a powerful tool for municipalities, but its efficacy and longevity depended on assessment quality, political framing, revenue horizons, and the wider economic conditions.

BC Assessment and the return of the land question

For several decades after B.C.’s early land-tax experiments, the centre of public finance shifted elsewhere. Income taxes, business taxes, and conventional property taxes came to dominate the revenue system. But the land question did not disappear. It returned in a new institutional form in the 1970s, with B.C.’s first NDP government and one of the most consequential land-policy ministers in the province’s history: Bob Williams.

Williams served as Minister of Lands, Forests and Water Resources from 1972 to 1975. During that period, B.C. created the modern assessment system that made timely, accurate, and uniform land-value assessment possible across the province.

The official BC Assessment history gives the institutional explanation. By 1973, B.C. had 140 independent assessment organizations using different valuation methods. Assessments were frequently challenged, difficult to defend, and increasingly seen as a serious provincial problem. In 1974, an all-party committee recommended a completely independent assessment authority.¹⁸

But the reform also belonged to a wider land-policy moment. Williams’ public policy ideas were shaped by Henry George’s view that land and resource values should be treated, at least in part, as common wealth. His commitment to George’s ideas made him controversial in some quarters. But as a self-described “socialist who believes in free enterprise,” Williams continued to argue that taxing land values was a more economically productive way to build the province.¹⁹

In his book, Using Power Well, Williams recounts how he recruited Mason Gaffney, one of the leading Georgist land economists of the twentieth century, to head an institute at the University of Victoria. In Gaffney, Williams found an adviser who shared his focus on economic rent and the public value embedded in land.²⁰

That connection led directly to Ted Gwartney, another central figure in the creation of B.C.’s modern assessment system. Gwartney later became Assessment Commissioner and Chief Executive Officer of the B.C. Assessment Authority. In his own account, his path began at the Henry George School in San Diego, where he studied the argument for replacing existing taxes with a charge on land rent. He later wrote that assessment work gave him a practical way to apply those ideas: to help communities “raise more revenue from land rather than from buildings.”²¹

In a tribute to Mason Gaffney, Gwartney recalled that Gaffney told him B.C. wanted to reform its assessment practices and “capture a greater proportion of public revenue from land and natural resources.” Gaffney arranged a meeting with Williams, then Minister of Lands, Forests and Water Resources, and Premier Dave Barrett. Gwartney was offered a one-year contract to advise B.C. on assessment reform.²²

Gwartney later wrote that he recommended a province-wide Assessment Authority independent of the taxing function, that the Authority was created in July 1974, and that he was appointed Assessment Commissioner and CEO later that year.²³

BC Assessment was not created to restore B.C.’s old land value tax system. Its formal purpose was uniform, independent, province-wide property assessment. But the people and ideas around its creation show that it was not merely a technical reform. For Williams, Gaffney, and Gwartney, accurate assessment was part of a larger land-policy project.

The logic was straightforward: before a province can tax land value, capture land lift, or build public support for either, it must first be able to measure land separately from buildings.

Gwartney’s later paper Estimating Land Values makes the point in practical terms. Land rent, he wrote, is the price paid for the exclusive use of a location. Because land is fixed in supply, taxing land does not reduce the supply of land. And if public action creates land value, the public has a claim to recover part of it.²⁴

The creation of the BC Assessment did not itself bring back Land Value Taxes. But it helped build the administrative infrastructure that any serious land-value policy would require: independent assessment, regular valuation, and a clear distinction between the value of land and the value of what people build on it.

Vancouver hosts the world, and land value capture enters the UN record

Two years after BC Assessment was created, Vancouver hosted Habitat I, the first United Nations Conference on Human Settlements.

The Vancouver Action Plan, adopted in 1976, included a striking section on land. It argued that land could not be treated like an ordinary asset because private control of land was a major instrument of wealth accumulation. It also called for public authorities to develop the tools needed to assess land values and return the “unearned increment” to the community.²⁸

Recommendation D.3, titled “Recapturing plus value,” made the point directly. It stated that increases in land value caused by public investment, changes in use, or community growth should be recaptured by public bodies. The recommended tools included land taxes, betterment charges, taxes on unused or under-used land, periodic assessment of land values, development charges, and public leasing.²⁹

It was a remarkable, if often overlooked, moment. Vancouver, once Canada’s most famous land value tax experiment, had become the host city for a global conference that placed land value capture at the centre of human settlements policy. The language had changed since the single-tax era, but the underlying principle was familiar: publicly created land value should, at least in part, return to the public.

The modern return: Victoria, UBCM, and Vancouver

By the 1980s, B.C.’s old land value tax system had given way to the current framework. Vancouver’s 2019 land value capture report states that since 1984, B.C. property tax has applied to 100 percent of land value and 100 percent of improvement value.³⁰

But the idea did not disappear. As land values rose and the housing crisis deepened, advocates and policymakers began looking again for tools that could curb speculation, encourage better use of land, and return more publicly created value to the public.

In 2017, Victoria brought a resolution to the Union of B.C. Municipalities calling for the restoration of local authority to introduce a land value tax. The resolution argued that LVT could encourage new housing and discourage the speculative holding of vacant property. UBCM endorsed it.³¹

The province responded that the municipal variable tax rate system does not allow land to be taxed separately from improvements. It also argued that vacant land is already assessed at its highest and best potential use.³²

Victoria returned to the issue in 2020 with another resolution, this time calling for municipalities to be able to tax land and improvements separately. UBCM endorsed that resolution as well.³³

The issue has continued to surface. In 2025, UBCM summarized its policy position as supporting vacant land taxation to help incentivize and fund affordable housing or shelters, along with greater local authority from the province. UBCM’s 2025 resolutions materials also show a longer trail of related endorsed resolutions, including proposals from 2007, 2008, 2011, 2017, 2020, 2021, and 2024.³⁴ ³⁵

Vancouver’s more recent work used the broader language of land value capture. In December 2018, council directed staff to examine existing tools such as Community Amenity Contributions and Development Cost Levies, consult BC Assessment, and explore how the city might collect a share of the land value created by public decisions.³⁶

The 2019 staff memo concluded that Vancouver already had a broad land value capture framework through DCLs, CACs, density bonusing, and property taxes. It also warned that a new recurring land value tax would require provincial legislative changes, assessment system changes, and coordination with the province, Metro Vancouver, and TransLink.³⁷

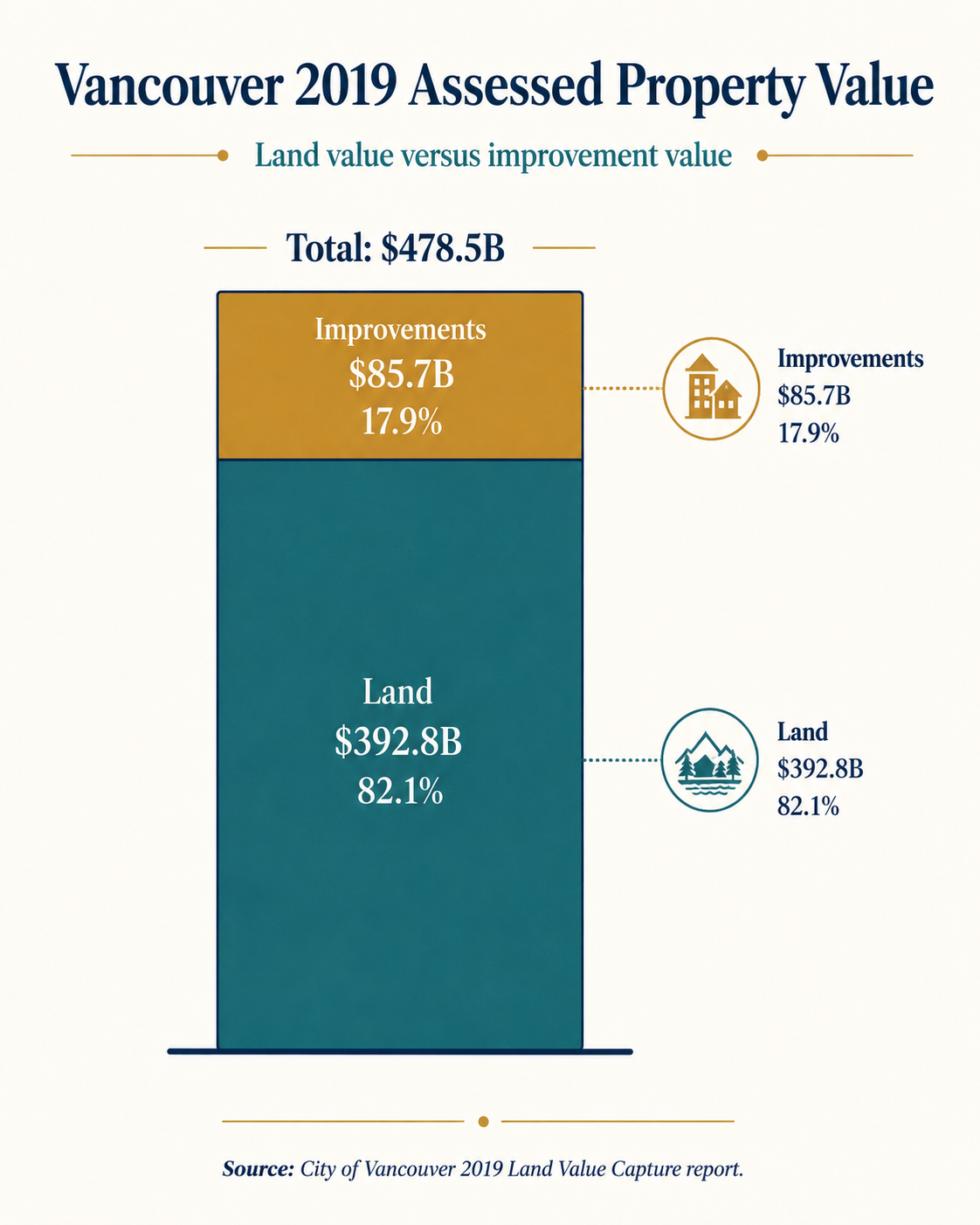

The consultant report gives one simple reason the issue keeps returning. In Vancouver’s 2019 assessment roll, land was assessed at roughly $392.8 billion. Improvements were assessed at about $85.7 billion.³⁸

In other words, most of the assessed value in the city was not in the buildings. It was in the land beneath them.

What this history tells us

B.C. has not forgotten land value taxation. It has renamed it, narrowed it, expanded it, abandoned it, rediscovered it, and embedded parts of it into the machinery of planning, assessment, and local finance.

The early vocabulary was the single tax. Later it became site-value taxation, actual-value assessment, land value capture, density bonusing, development charges, CACs, vacant land taxation, and municipal fiscal authority.

But the core question has barely changed:

When public decisions create private land wealth, how much of that wealth should return to the public?

British Columbia has been asking that question for more than a century.

It asked it in the 1890s, when municipalities began separating land from improvements.

It asked it in 1910, when Vancouver shifted taxation toward land.

It asked it in 1974, when the province created BC Assessment.

It asked it in 1976, when the world came to Vancouver for Habitat I.

And it is asking it again now, through housing affordability, speculation, transit investment, public infrastructure, and the search for new local revenue tools.

The policy has never been simple. Its history is full of qualifications. B.C.’s early land value taxes were not pure Georgism. BC Assessment was not created solely for land value taxation. CACs and DCLs are not simply LVT. And modern Land Value Return policies would require legislative change, careful design, clear assessment rules, and a credible plan for transition.

But the history is also clear on something else.

British Columbia has already built much of the intellectual, political, and administrative foundation for this conversation. The province has done versions of this before. In a time when land values are once again driving inequality, housing unaffordability, and rising public costs, that history deserves to be remembered and lived up to.

Sources

¹ Mohammad Qadeer and Andrejs Skaburskis, Recapturing of Unearned Increments, Land Taxes and Betterment Levies, CMHC, 1994.

² City of Vancouver, 2018 council motion included in the 2019 Land Value Capture report.

³ Archibald Stalker, Taxation of Land Values in Western Canada, McGill University thesis, 1913/1914.

⁴ BC Assessment history page; Vaughn Palmer review of Using Power Well; Henry George Foundation of Canada review; Ted Gwartney, The Potential of Public Value.

⁵ Habitat I, Vancouver Action Plan, Recommendation D.3, 'Recapturing plus value.'

⁶ UBCM records for Victoria’s 2017 and 2020 resolutions and UBCM’s 2025 policy position on vacant land taxation.

⁷ Henry George, Progress and Poverty, 1879; Stalker, Taxation of Land Values in Western Canada.

⁸ Stalker, Taxation of Land Values in Western Canada, introduction.

⁹ Thomas Robert Loosmore, The British Columbia Labor Movement and Political Action, 1879-1906, UBC thesis, 1954.

¹⁰ Stalker, Taxation of Land Values in Western Canada, Chapter II.

¹¹ Qadeer and Skaburskis, CMHC, 1994.

¹² Stalker, Taxation of Land Values in Western Canada.

¹³ City of Vancouver, 2018 Land Value Capture motion.

¹⁴ Stalker, Taxation of Land Values in Western Canada, conclusion.

¹⁵ Stalker’s Vancouver revenue table.

¹⁶ Stalker’s discussion of Vancouver’s 1913 revenue pressures.

¹⁷ Qadeer and Skaburskis, CMHC, 1994.

¹⁸ BC Assessment history: https://info.bcassessment.ca/About-Us/about-BC-Assessment/history

¹⁹ Vaughn Palmer, Vancouver Sun review of Using Power Well: https://cooperative-individualism.org/palmer-vaughn_a-remembrance-of-bob-williams-2022-jul-2.pdf

²⁰ Henry George Foundation of Canada review of Using Power Well: https://earthsharing.ca/news/using-power-well

²¹ Henry George Foundation of Canada review of Using Power Well: https://earthsharing.ca/news/using-power-well

²² Jim Green Foundation video page: https://vimeo.com/247219329; BC Co-operative Association memoriam.

²³ Ted Gwartney, The Potential of Public Value: https://www.cooperative-individualism.org/gwartney-ted_potential-of-public-value.pdf

²⁴ Ted Gwartney tribute to Mason Gaffney: https://masongaffney.org/tributes.html

²⁵ Ted Gwartney, The Potential of Public Value: https://www.cooperative-individualism.org/gwartney-ted_potential-of-public-value.pdf

²⁶ Ted Gwartney, Estimating Land Values, 1999.

²⁷ Ted Gwartney, Estimating Land Values, 1999.

²⁸ Habitat I, Vancouver Action Plan, Land Preamble: https://habitat76.ca/2016/06/un-habitat-1976-vancouver-declaration-action-plan/

²⁹ Habitat I, Vancouver Action Plan, Recommendation D.3: https://habitat76.ca/2016/06/un-habitat-1976-vancouver-declaration-action-plan/

³⁰ City of Vancouver, 2019 Land Value Capture report.

³¹ UBCM Resolution B14, Restoration of Land Value Tax, 2017: https://www.ubcm.ca/convention-resolutions/resolutions/resolutions-database/restoration-land-value-tax

³² Provincial response to UBCM 2017-B14: https://www.ubcm.ca/convention-resolutions/resolutions/resolutions-database/restoration-land-value-tax

³³ UBCM Resolution EB44, Tax Land and Improvements Separately, 2020: https://www.ubcm.ca/convention-resolutions/resolutions/resolutions-database/tax-land-and-improvements-separately

³⁴ UBCM policy position on vacant land taxation, January 29, 2025: https://www.ubcm.ca/about-ubcm/latest-news/ubcm-policy-position-vacant-land-taxation

³⁵ UBCM 2025 Resolutions Book: https://www.ubcm.ca/sites/default/files/2025-08/2025%20UBCM%20Resolutions%20Book.pdf

³⁶ Vancouver’s 2018 Land Value Capture motion.

³⁷ Vancouver’s 2019 staff memo and WMCI discussion paper.

³⁸ Vancouver’s 2019 Land Value Capture report, Exhibit 4, total assessed value of land and improvements.